If you are new to investing, you may find market corrections scary. However, these can be perfect opportunities to buy stocks that otherwise look expensive. As of this writing, the Nasdaq Composite Index has corrected roughly 21% this year.

High-flying electric vehicle (EV) stocks too have fallen significantly. Let’s focus on three EV stocks that look appealing right now.

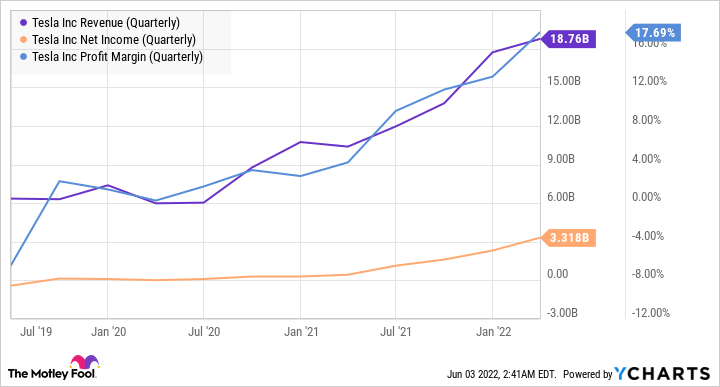

1. Tesla

Investors had long been divided on Tesla‘s (TSLA 1.98%) success as an EV maker. However, with growing revenues, profits, and margins over the past several quarters, the company has put some of those arguments behind it.

TSLA Revenue (Quarterly) data by YCharts

The debate has instead now shifted to the high valuation of Tesla stock. With a price-to-earnings (P/E) ratio of 105, the stock gives a solid reason to support this claim. Even based on forward earnings, the ratio at nearly 63 is high.

TSLA PE Ratio data by YCharts.

Even then, it is a dramatic improvement from a P/E ratio of above 600 that the stock sported a year ago. Similarly, Tesla’s price-to-sales (P/S) ratio of around 14 right now is well below its average ratio of nearly 20 in the last one year. In November, the P/S ratio was nearly 30.

Tesla has managed to carve a place for itself in a capital-intensive business with high barriers to entry. Moreover, it has lately been generating industry-leading margins. Tesla’s CEO Elon Musk plans to cut some jobs anticipating a weaker economy. This move again could be an attempt to keep margins from falling, in case a slowdown indeed comes. Finally, there are several growth avenues for Tesla other than electric vehicles. What it shows is that even if Tesla stock doesn’t reach to its historical P/E or P/S ratios, there is some scope for multiple expansion from their current levels. Further, earnings and sales growth will support the stock’s price, even if the multiples don’t rise from their current levels.

Overall, Tesla stock is looking far more attractive now than it was at the start of the year. If you’ve been looking to buy the stock, now could be a good time.

2. Rivian

Rivian (RIVN 0.63%) stock has fallen roughly 69% so far this year. A broader market correction has hurt this young EV maker more than other comparable companies as investors are avoiding more speculative companies. The euphoria surrounding Rivian sent the stock’s price to unsustainable levels soon after it went public in November last year.

Image source: Rivian.

Rivian has not yet achieved profitable operations. What’s more, supply chain challenges and higher materials cost are further hurting the company’s performance. Scaling up profitably remains a key challenge for Rivian. Obviously, investors are concerned, causing a sell-off in the stock.

However, there are some key positives about Rivian that the market is ignoring. The company is an early mover in the key electric pickup truck segment, and its products have broadly received positive reviews. It also has a big order for electric delivery vans from Amazon. So, a lack of demand isn’t a concern for Rivian. As a new EV maker, Rivian is bound to face challenges, but it can eventually navigate through these.

Overall, Rivian stock has fallen to more attractive levels. Based on estimated sales for the next fiscal year, Rivian’s forward P/S ratio is roughly 4. Although it looks high, the company is just starting and has years of growth ahead.

Considering that the stock’s price has been wildly fluctuating and that the company is not yet profitable, it is important to bear in mind that the stock is suitable only for investors with a high appetite for risk.

3. ChargePoint

ChargePoint (CHPT 2.81%) reported earnings for its fiscal quarter ending April 30 last week. The company’s revenue more than doubled from the year-ago quarter. But its loss from operations also widened from $46.6 million to $89.8 million. The company attributed the growing losses mainly to supply chain disruptions, which resulted in higher costs.

Looking beyond the latest quarter results, like other EV charging providers, ChargePoint’s business model is still unproven. Unlike gas stations, EV charging companies cannot become profitable selling electricity. Rather, ChargePoint sells its chargers, subscriptions, and warranty services to commercial customers, such as workplaces, retail locations, and parking operators, who offer these as a perk to employees or use them to attract customers. ChargePoint also targets residential customers as well as fleet operators looking to electrify their fleets.

How ChargePoint’s business evolves over time remains to be seen. Yet, if you’re willing to take the associated risks, ChargePoint looks like the best bet among EV charging companies. ChargePoint stock’s forward P/S ratio is lower than that for its listed peers Blink Charging and EVgo. Moreover, the stock is 70% off its all-time high price, offering an attractive entry point for long-term investors.

George is Digismak’s reported cum editor with 13 years of experience in Journalism